THE PROGRAMMATIC HAMMER vs. THE AGENTIC NAIL

Why treating AI marketing as an impressions transaction engine could be the most expensive mistake brands make

When you’re a hammer, everything looks like a nail. When you’ve spent your career in programmatic advertising, everything looks like an impressions transaction — including agentic marketing. But from our work with brands, agencies, publishers, and technology platforms, we can tell you plainly: Anyone who brings that programmatic hammer to the agentic marketplace risks building a house of cards.

The establishment view holds that the primary agentic use case is making programmatic media procurement smarter. Agentic AI, they say, is an optimization layer on top of existing infrastructure, not a disruption of it. DSPs and SSPs will be fine. Agency holding companies will evolve into systems integrators. Existing technical standards can be adapted for AI environments. And major agency acquisitions of identity infrastructure are honest, forward-looking agentic investments, rather than targeted moves to control the critical infrastructure brands require.

That programmatic lens is distorting what’s happening across the full breadth of the marketing supply chain. To understand why, it helps to understand how the agentic marketplace is actually organizing itself.

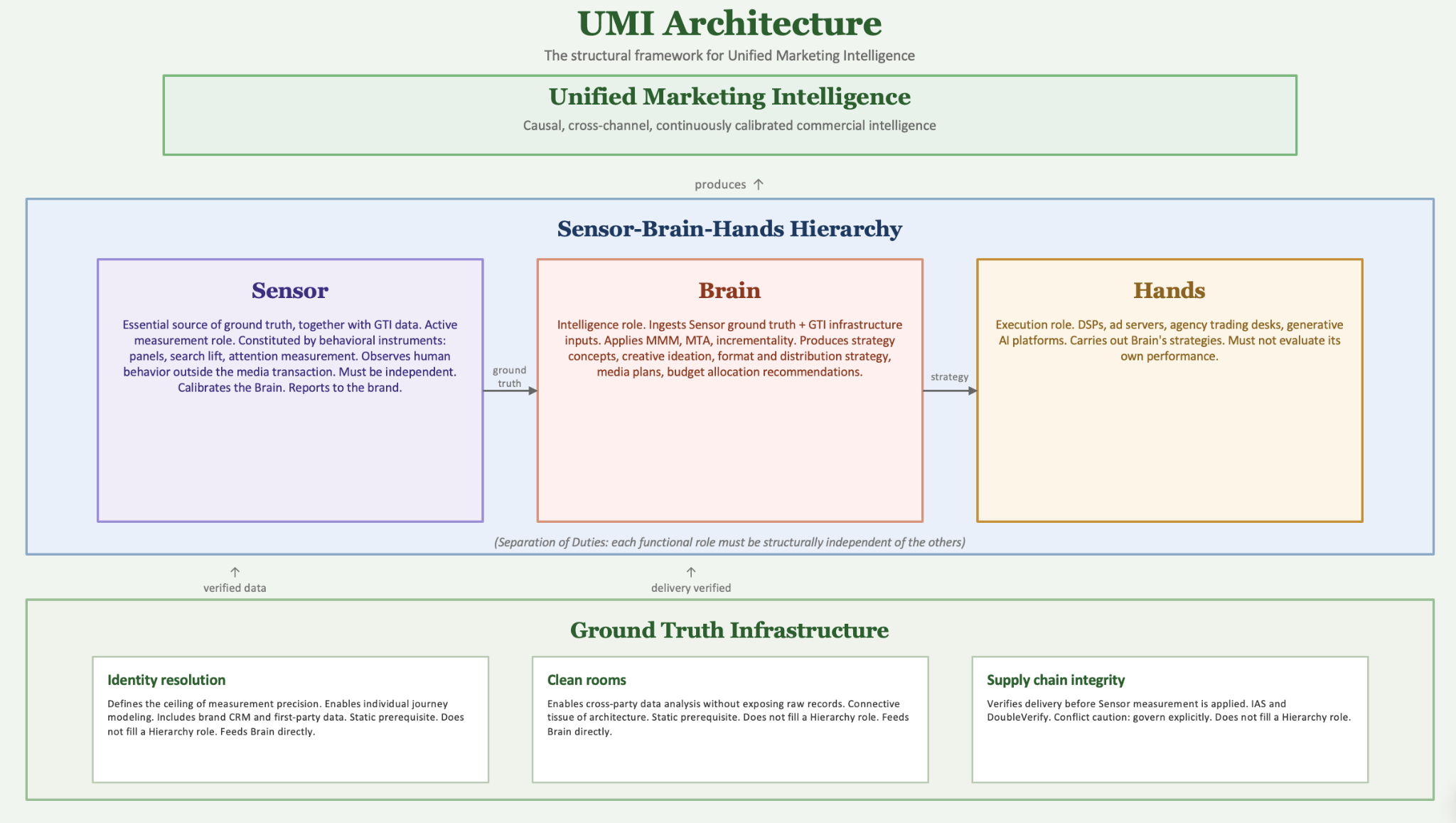

Unified Marketing Intelligence

The emerging architecture — what we call Unified Marketing Intelligence, or UMI — is structured around a three-layer taxonomy, Sensor→Brain→Hands, built on top of an unimpeachable Ground Truth Infrastructure (see illustration, “UMI Architecture”). The Ground Truth bedrock is the deterministic identity data foundation that anchors the system. The Sensor layer consists of independent measurement instruments that read real-world behavioral signals, without a financial stake in the outcome. The Brain layer is the AI-native intelligence that synthesizes those signals into strategy, planning, and optimization. The Hands layer is where decisions are carried into the market — the execution platforms, agencies, and trading systems. And what is being optimized isn’t just formatted ad inventory, but creative content that delivers on the brief in ways that best engage the brand’s target personas, driving a much bigger lift in ROI than better targeting alone.

The Unified Marketing Intelligence that comprises these capabilities is not a product. It is the organizing logic of the agentic marketing era, and it represents by far the most consequential impact of AI on marketing, because it levels the playing field in ways that were structurally impossible before. The intelligence that used to require a holding company’s decades of accumulated data and institutional knowledge can now be assembled independently, at a fraction of the cost, by any organization willing to build the right architecture. Boutique creative agencies can now compete with giant holdcos. Brands can insource capabilities for which they historically relied on external contractors.

From our own work with clients, the most vital early agentic use cases are upstream of the media buy. Autonomous scenario modeling for marketing mix allocation. AI-assisted competitive intelligence synthesis. Agentic synthesis of real-time behavioral signals as an input into the brief, to optimize the matching of creative content to the right personas with the right copy and imagery. Creative development systems that generate, test, and iterate creative variety tailored to those personas faster than any human team can on their own.

As we documented in our recent work on AI change management, marketing has been organized for more than a century around a linear assembly line — brief, copy, design, media plan, media buy, measurement. AI’s most profound effect is not automating that line; it is dissolving the line entirely, shifting the organization from manual authorship to orchestration of dynamic systems that adapt in real time.

That shift is happening in strategy, planning, and creative well before the work reaches the trading desk. The media buy is the last mile. Focusing agentic AI exclusively there, while other functions undergo equivalently significant transformation, is a defense of a very particular present play-acting as a vision of the future. AsTom Chavez, an ad tech veteran and founder of the AI strategy platform Kana, likes to say: “You cannot pave the cow path.”

Brands & Publishers

One of the clearest signals that agentic marketing extends well beyond programmatic optimization comes from publishers and brands themselves. To them, the appeal of agentic intermediation is not that it makes programmatic trading more efficient. It is that it helps them escape programmatic’s logic entirely.

Programmatic trading has been an engine of commoditization for publishers and brands: It compresses CPMs, privileges inventory scale over editorial quality, and reduces the relationship between brand and publisher to a price-per-impression negotiation in which the publisher almost always loses and the publisher’s relationships with consumers, forged through the power of differentiated content, are devalued.

Agentic media buying is being designed to bypass the programmatic workflow and its substantial intermediary costs. For publishers, agentic is not about smarter bidding. It is about being found and valued for things an auction market was never capable of pricing. Autonomous agents, reasoning from brand objectives rather than from auction mechanics, can discover and evaluate forms of marketing support from publishers that cannot be traded programmatically at all: branded content partnerships, audience intelligence collaborations, sponsored editorial franchises, research co-investment, and more.

That prospect will almost certainly disrupt the buy-side and sell-side platforms, as the market is showing. Omnicom has already executed live media buys for several clients through an agent-to-agent framework, with software autonomously purchasing ad inventory directly from publishers and skirting the ad tech intermediaries. PubMatic and Butler/Till launched the industry’s first fully autonomous CTV campaign in December 2025. Ad Context Protocol (AdCP) is designed specifically for direct deals and programmatic guaranteed, supporting a multi-step conversation between brand and publisher agents that writes transactions directly into an ad server — often end-running the traditional bidstream entirely. The IAB Tech Lab’s Agentic Real-Time Framework (ARTF), supported by the Trade Desk, Amazon, Index Exchange, and others, is working to restructure the RTB infrastructure itself to accommodate agentic workflows.

This doesn’t mean DSPs and SSPs disappear. It means the business logic sustaining their current form — and their current margin structures — is under genuine competitive pressure for the first time in nearly 20 years.

Where Standards Matter

Much of that pressure is coming from the primaries in the marketing-media ecosystem that were pushed into corners by the programmatic revolution. Brands are insourcing their own UMI stacks. Small marketing startups like Vibe.co and MNTN are agentifying end-to-end agency workflows and bringing SMBs into a television advertising ecosystem they could not afford historically.

They can do this because agentic intermediation renders much of the complexity of programmatic advertising transparent, even invisible. Without question, shared technical protocols like AdCP and ARTF remain necessary for harmonizing multi-step agentic advertising workflows – essentially agentifying the Hands layer of the UMI stack. But The Brain layer no longer requires arduous, political, years-long negotiations to create industry-wide taxonomies, data dictionaries, and measurement schema: LLMs can use semantic normalization to automatically reconcile inconsistent data structures across CRM systems, media logs, retail transactions, call centers, survey data, and more — enabling analyses across thousands of previously incompatible marketing datasets without requiring shared blueprints. What once required months of manual reconciliation can now be done in hours by a non-technical user describing a data need in plain language.

Can Holdcos Hold?

And this is why the holding companies’ evolution into systems integrators will be anything but easy.

The Nobel Prize-winning economist Ronald Coase argued that vertical integration persists in an industry as long as the cost of coordinating across independent suppliers exceeds the cost of owning them. The advertising holdcos did not merely benefit from coordination complexity, they cultivated it, and the information asymmetry they manufactured across the marketing supply chain is precisely what AI-enabled transparency is now dissolving.

To fight back, the holdcos are relying on their 40-year consolidation playbook. Publicis has assembled the most ambitious attempt yet to own three layers simultaneously — Ground Truth Infrastructure, Brain, and Hands — through a decade of acquisitions culminating in its purchase of LiveRamp. Omnicom’s absorption of IPG is explicitly framed as creating the data and technology scale to compete in an AI-driven market. The bundling of measurement, intelligence, and execution hasn’t been abandoned by the large agencies. It has, if anything, accelerated.

But acceleration in a particular direction doesn’t mean the holdcos are heading in the right direction — for themselves, or their clients.

Owning data and controlling media procurement is no longer sufficient to defend or grow the value that agencies provide brands. The AI era rewards agencies that can demonstrate irreplaceable intelligence — genuine insight generation, strategic synthesis, creative vision — across the full UMI architecture. It does not reward agencies simply for sitting between brands and the media supply chain, however sophisticated the plumbing they’ve assembled around that position.

Some agency incumbents are embracing this change. “We have built out an end-to-end marketing intelligence engine that is smarter than any human, that is doing work in minutes that literally used to take months,” Horizon CEO Bill Koenigsberg has said of the media-buying behemoth’s construction of BLU, an integrated UMI platform.

The larger holding companies, though, are being outflanked on all sides simultaneously. From below, AI platforms are turning services into software — automating the analytical and optimization work that agencies have historically charged for as labor. From above, brands that build their own UMI stacks are discovering they can insource capabilities that once required agency relationships. From the side, disruptive players are filling the intelligence gaps that holding companies are moving too slowly to close.

The market data provides unsparing evidence of the holdcos’ challenges. WPP has lost nearly two-thirds of its market value since the start of 2025, falling from approximately $11 billion to roughly $3.8 billion today. Accenture Song won a $100 million media management account from WPP and IPG in June 2025 — proof that the consulting firms that were largely foreclosed from agency economics for two decades are now viable competitors, precisely because AI has eroded the proprietary data advantages holdcos spent thirty years accumulating. Brandtech Group reached $1 billion in revenue and a $4 billion valuation without a traditional programmatic trading desk.

Brands remain deeply reliant on agency partners — that reliance is real, and we don’t expect it to evaporate. But the nature of the value those partners must provide is changing faster than most holdco organizational structures can accommodate. Agencies that thrive in the UMI era will be those that earn their position in the Brain layer through genuine intelligence contribution, not those that defend their position in the Hands layer by controlling data flows and procurement infrastructure. The latter strategy buys time. It does not build a durable competitive moat in an era where the intelligence function is the prize.

Conflicting Advice

Whether brands capitalize on the modular UMI architecture appearing in the market to build their own intelligence and execution stacks depends on their risk tolerance. As autonomous agents increasingly make creative and budget allocation decisions at machine speed, the quality of the Ground Truth those decisions are calibrated against becomes existentially consequential. In agentic AI systems, tiny errors propagate through interconnected systems, rapidly snowballing into large-scale distortion and creating, as Deloitte has documented, “a chain of compounded errors in which small inaccuracies at each step accumulate into large-scale distortion of business processes and decisions.”

Against that backdrop, the consolidations sweeping the marketing-media ecosystem — agency acquisitions of identity infrastructure, DSPs and SSPs absorbing measurement platforms — look potentially more destructive than the garden variety “grading-their-own-homework” conflicts brands have ignored for decades from their partners.

Five Predictions

Nothing about agentic marketing will be business as usual. The promise of Unified Marketing Intelligence will unsettle - and, we expect, excite - every denizen of the ecosystem, as brands and their partners grab at the opportunities AI tools now offer:

Brands will insource more of the capabilities for which they historically relied on agencies and other suppliers, ranging from marketing strategy to creative development to measurement of outcomes.

As AI bots lower agencies’ and publishers’ cost-to-serve, their growth increasingly will derive from mid-market brands that in earlier decades proved too expensive to serve.

The M&A wave will accelerate, as value chain roles blur; the information asymmetry that protected holdcos, currency setters, and DSPs erodes; and players stake out strategic bets across the Ground Truth Infrastructure-Sensor-Brain-Hands hierarchy.

Brands will take more critical looks at the “grading-their-own- homework” conflicts that degrade the Ground Truth data on which their intelligence architecture depends.

Company leaders, inside and outside the marketing function, will spend more time managing change, as their teams grapple with transforming from administrators of handoffs to orchestrators of value creation.

The hammer is a useful tool. It built the programmatic marketplace that delivered real value for two decades. But you cannot frame a house with just a hammer. When the job changes, so must the tools. UMI makes possible a marketing intelligence architecture that works for brands, strategic agencies, publishers, and tech contributors rather than for the intermediaries who have historically extracted value from them.

Matthew Egol is the founder and CEO of JourneySpark Consulting and a specialist in AI-era organizational transformation. John Frelinghuysen is the founder of Frelinghuysen Advisors and a veteran strategy advisor to brand marketers and investors. Randall Rothenberg served for 15 years as CEO of the IAB and is a longtime marketing-media executive and consultant. Their ongoing research on Unified Marketing Intelligence examines the structural transformation of the marketing-advertising supply chain.

| A guest post by

|

I'd separate semantic interoperability from economic trust. LLMs are incredibly good at answering "what does this data mean?" I'm more interested in what happens after meaning is established: Who authorized the action, under what authority, within what scope, and who is accountable for the outcome? That's where I suspect the next generation of standards emerges.